Last month, 73.4 percent of Las Vegas-area homes and condos that were resold had been previously foreclosed on in the prior 12 months, according to DataQuick.

That’s up from the 55.9 percent share that was distressed a year earlier, a sign that the crisis is far from over.

The only good news (if you want to call it that), is that sales are up, with 4,536 new and resale homes and condos closing escrow during the month, up 1.9 percent from April and 23 percent from a year ago.

To view original article click here

Other good articles...

JPMorgan Tightens Grip on Equity Sales by Selling Own Shares

...helped by the sale of shares of financial firms, including their own.

Paper Avalanche Buries Plan to Stem Foreclosures

Think of the documents as being part of a pile massing inside the bank

Recovery threatened by toxic assets still hidden in key banks

Governments too slow to act, warn

Toxic Assets (PPIP) Death Rattle

Remember, folks, that the DOW surged by more than 500 points, a 7% gain, on the day the PPIP was announced.

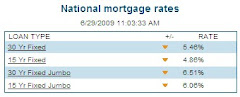

Monday, June 29, 2009

Friday, June 26, 2009

JPMorgan, Citigroup Expand in ‘Jumbo’ Loans for Expensive Homes

June 26 (Bloomberg) -- JPMorgan Chase & Co. and Citigroup Inc. are expanding in “jumbo” mortgages used to buy the most expensive homes, helping revive a market that shriveled amid a three-year jump in homeowner defaults.

JPMorgan resumed buying new jumbo loans made by other lenders this month, after halting purchases in March, spokesman Tom Kelly said. Borrowers must have checking accounts with the bank, he said. Citigroup is again offering the loans through independent mortgage brokers, spokesman Mark Rodgers said.

The two New York-based banks are signaling new interest in a market hobbled since 2007, when record-breaking defaults on home loans caused investors to flee securities backed by mortgages. With the recession sapping demand for new consumer and corporate loans, lenders are competing harder for creditworthy customers, said Harry Davis, banking professor at Appalachian State University in Boone, North Carolina.

“They have surely across the board raised lending standards, and there aren’t a lot of good borrowers standing in the lobby,” Davis said in an interview.

To read the original article click here

Other interesting articles...

Loan Modifications Up at Fannie, Freddie, But So Are Late Payments

Loan modifications at Fannie Mae and Freddie Mac were up 57 percent in the first quarter

41 Charges as Mortgage Fraud Hits Condos & Suburbs

Federal law enforcement officials recently announced charges have brought against 41 defendants in five separate cases in Chicago.

REQUIRED READING: The Fannie And Freddie Quandary

It's a perfect time to think about the fundamental restructuring of the world famous (and now broke) government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac.

Rep. Issa Says Fed ‘Engaged in a Cover-Up’ on Merrill-Bofa

U.S. Congressman Darrell Issa said the Federal Reserve “engaged in a cover-up”

JPMorgan resumed buying new jumbo loans made by other lenders this month, after halting purchases in March, spokesman Tom Kelly said. Borrowers must have checking accounts with the bank, he said. Citigroup is again offering the loans through independent mortgage brokers, spokesman Mark Rodgers said.

The two New York-based banks are signaling new interest in a market hobbled since 2007, when record-breaking defaults on home loans caused investors to flee securities backed by mortgages. With the recession sapping demand for new consumer and corporate loans, lenders are competing harder for creditworthy customers, said Harry Davis, banking professor at Appalachian State University in Boone, North Carolina.

“They have surely across the board raised lending standards, and there aren’t a lot of good borrowers standing in the lobby,” Davis said in an interview.

To read the original article click here

Other interesting articles...

Loan Modifications Up at Fannie, Freddie, But So Are Late Payments

Loan modifications at Fannie Mae and Freddie Mac were up 57 percent in the first quarter

41 Charges as Mortgage Fraud Hits Condos & Suburbs

Federal law enforcement officials recently announced charges have brought against 41 defendants in five separate cases in Chicago.

REQUIRED READING: The Fannie And Freddie Quandary

It's a perfect time to think about the fundamental restructuring of the world famous (and now broke) government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac.

Rep. Issa Says Fed ‘Engaged in a Cover-Up’ on Merrill-Bofa

U.S. Congressman Darrell Issa said the Federal Reserve “engaged in a cover-up”

Wednesday, June 24, 2009

Not Paying the Mortgage, Yet Stuck With the Keys

Foreclosure Backlog Imperils Recovery

A growing number of American homeowners are falling into financial limbo: They're badly behind on payments, but their banks have not yet foreclosed.

The backlog of seriously delinquent mortgages, which so far affects about 1 million borrowers, is a shadow over hopes for a rebound in the nation's housing markets. It masks the full extent of the foreclosure crisis and threatens to depress prices even further just as some parts of the country are hinting at recovery. For lenders, it could portend even more financial losses tied to the mortgage meltdown.

"It just means foreclosure rates are going to keep rising," said Patrick Newport, an economist for IHS Global Insight.

Rising mortgage delinquencies were at the root of the recession, and many economists say an economic recovery will be difficult until the housing market recovers and home prices stabilize.

And even though a delayed foreclosure can be a blessing for some troubled homeowners, for others, it simply prolongs the financial distress, leaving them on the hook for the condition of the property. Even if they move out, they cannot move on.

To read the entire article click here

Other interesting articles...

Citigroup Halts Some Mortgage Applications, Cites Missing

DataCitigroup Inc. suspended loan applications at a unit that produced half of its $115 billion in mortgages last year

Banks Oppose Financial Agency; Consumers Seek Clarity

U.S. bankers lined up against a new federal oversight agency proposed by President Barack Obama,

A growing number of American homeowners are falling into financial limbo: They're badly behind on payments, but their banks have not yet foreclosed.

The backlog of seriously delinquent mortgages, which so far affects about 1 million borrowers, is a shadow over hopes for a rebound in the nation's housing markets. It masks the full extent of the foreclosure crisis and threatens to depress prices even further just as some parts of the country are hinting at recovery. For lenders, it could portend even more financial losses tied to the mortgage meltdown.

"It just means foreclosure rates are going to keep rising," said Patrick Newport, an economist for IHS Global Insight.

Rising mortgage delinquencies were at the root of the recession, and many economists say an economic recovery will be difficult until the housing market recovers and home prices stabilize.

And even though a delayed foreclosure can be a blessing for some troubled homeowners, for others, it simply prolongs the financial distress, leaving them on the hook for the condition of the property. Even if they move out, they cannot move on.

To read the entire article click here

Other interesting articles...

Citigroup Halts Some Mortgage Applications, Cites Missing

DataCitigroup Inc. suspended loan applications at a unit that produced half of its $115 billion in mortgages last year

Banks Oppose Financial Agency; Consumers Seek Clarity

U.S. bankers lined up against a new federal oversight agency proposed by President Barack Obama,

Tuesday, June 23, 2009

May existing home sales rose 2.4 percent

Existing home sales rose 2.4 percent in May; prices plunge 16.8 percent

By Alan Zibel, AP Real Estate Writer

On Tuesday June 23, 2009, 10:40 am EDT

WASHINGTON (AP) -- Sales of previously occupied homes rose modestly from April to May, the third monthly increase this year, but signs of a housing recovery are fragile at best. The National Association of Realtors said Tuesday that home sales rose 2.4 percent last month to a seasonally adjusted annual rate of 4.77 million, from a downwardly revised pace of 4.66 million in April.

About one out of every three homes sold was a foreclosure or distressed sale. That helped drag down the median price to $173,000 -- 16.8 percent below a year ago.

Falling prices coupled with new rules for property appraisers have caused many transactions to fall apart or be delayed.

"We have just been flooded with e-mails, telephone calls on the appraisal problems," said Lawrence Yun, the Realtors' chief economist.

To read the original article click here

You may also want to read...

S&P Downgrades More U.S. Prime Jumbo RMBS

Economic Crisis Stirs Free-Market Debate

U.S. Economy: Slide in Home Prices Spurs Increase in Resales

By Alan Zibel, AP Real Estate Writer

On Tuesday June 23, 2009, 10:40 am EDT

WASHINGTON (AP) -- Sales of previously occupied homes rose modestly from April to May, the third monthly increase this year, but signs of a housing recovery are fragile at best. The National Association of Realtors said Tuesday that home sales rose 2.4 percent last month to a seasonally adjusted annual rate of 4.77 million, from a downwardly revised pace of 4.66 million in April.

About one out of every three homes sold was a foreclosure or distressed sale. That helped drag down the median price to $173,000 -- 16.8 percent below a year ago.

Falling prices coupled with new rules for property appraisers have caused many transactions to fall apart or be delayed.

"We have just been flooded with e-mails, telephone calls on the appraisal problems," said Lawrence Yun, the Realtors' chief economist.

To read the original article click here

You may also want to read...

S&P Downgrades More U.S. Prime Jumbo RMBS

Economic Crisis Stirs Free-Market Debate

U.S. Economy: Slide in Home Prices Spurs Increase in Resales

Monday, June 22, 2009

Fed plans repo markets revamp

By Henny Sender and Michael Mackenzie in New York

Published: June 21 2009 22:31 Last updated: June 21 2009 22:31

The US Federal Reserve is considering dramatic changes to the giant repurchase – or repo – markets where banks around the world raise overnight dollar loans.

The plans include creating a utility to replace the Wall Street banks that handle transactions, people familiar with the matter say.

The Fed’s deliberations are partly motivated by concerns that the structure of the US overnight repurchase market may have exacerbated the financial turmoil that accompanied the failure of Lehman Brothers in September last year.

Fed officials plan to meet next month with market participants to discuss reforms.

People familiar with the Fed’s thinking say it is looking into the creation of a mechanism to replace the clearing banks – the biggest of which are JPMorgan Chase and Bank of New York Mellon – that serve as intermediaries between borrowers and lenders.

“The Fed is raising questions about whether the system really protects the interests of all participants,” says one person familiar with the Fed’s thinking.

In the repo markets, borrowers, such as banks, pledge collateral in return for overnight loans from lenders, such as money market funds.

To read the original article click here

You may also want to read...

Making Home Affordable program may help more underwater homeowners

The Making Home Affordable program may be further expanded to help more underwater homeowners refinance their mortgages.

FHA warns it may need assistance top operate

The FHA continues to be overwhelmed by surging loan volume, as evidenced by remarks from Kenneth M. Donohue, Inspector General of HUD.

No recovery for U.S. property markets until 2017

The U.S. urban commercial real estate markets probably will not recover until 2017

Fed meeting gets underway

The Federal Open Market Committee begins a two-day meeting on interest rate policy.

Published: June 21 2009 22:31 Last updated: June 21 2009 22:31

The US Federal Reserve is considering dramatic changes to the giant repurchase – or repo – markets where banks around the world raise overnight dollar loans.

The plans include creating a utility to replace the Wall Street banks that handle transactions, people familiar with the matter say.

The Fed’s deliberations are partly motivated by concerns that the structure of the US overnight repurchase market may have exacerbated the financial turmoil that accompanied the failure of Lehman Brothers in September last year.

Fed officials plan to meet next month with market participants to discuss reforms.

People familiar with the Fed’s thinking say it is looking into the creation of a mechanism to replace the clearing banks – the biggest of which are JPMorgan Chase and Bank of New York Mellon – that serve as intermediaries between borrowers and lenders.

“The Fed is raising questions about whether the system really protects the interests of all participants,” says one person familiar with the Fed’s thinking.

In the repo markets, borrowers, such as banks, pledge collateral in return for overnight loans from lenders, such as money market funds.

To read the original article click here

You may also want to read...

Making Home Affordable program may help more underwater homeowners

The Making Home Affordable program may be further expanded to help more underwater homeowners refinance their mortgages.

FHA warns it may need assistance top operate

The FHA continues to be overwhelmed by surging loan volume, as evidenced by remarks from Kenneth M. Donohue, Inspector General of HUD.

No recovery for U.S. property markets until 2017

The U.S. urban commercial real estate markets probably will not recover until 2017

Fed meeting gets underway

The Federal Open Market Committee begins a two-day meeting on interest rate policy.

Friday, June 19, 2009

Rates Fall Back on Lower Inflation

By DIANA GOLOBAY June 18, 2009 10:39 AM CST

Average mortgage rates across the board fell in the week ending June 18 after spiking briefly the week before, according to a survey released today by mortgage giant Freddie Mac (FRE: 0.7353 +2.12%).

“Reports of benign inflation figures reversed the upward trend of mortgage rates this week,” however, “it’s still too early to tell whether the decline in housing market activity has hit bottom yet,” says Frank Nothaft, Freddie’s chief economist, in a media statement today.

Thirty-year fixed mortgages (FRMs) averaged 5.38% rates with an average 0.7 point, down from 5.59% last week. The average rate for a 15-year FRM came in at 4.89% with an average 0.7 point, from 5.06% last week. Five-year adjustable-rate mortgages (ARMs) averaged 4.97% with an average 0.6 point, from 5.17% last week, while one-year ARMs averaged 4.95% with an average 0.6 point, from 5.19% the week before.

A separate survey conducted by Bankrate.com confirmed a drop in rates, with 30-year FRMs averaging 5.76% with an average 0.43 point, down from 5.96% the previous week. Bankrate’s data also found 15-year FRMs down to 5.19% from 5.37%.

“The concerns about eventual inflation that drove bond yields and mortgage rates higher have been tempered by the reality of continued weakness in the economy,” Bankrate said in a media statement.

To read the original article click here

Additional articles of interest...

Originate to Distribute Mortgages Default More

Mortgages sold on the secondary market quickly after being originated were underwritten more poorly than loans kept on bank’s books, according to a report from the University of Michigan Ross School of Business.

We’ve Gone From Saving Wall Street in Order to Save Main Street to Just Saving Wall Street

But parsing through his 85-page plan, it's not clear how these reforms will ensure that our financial system works for the economy as a whole.

Wall Street isn’t buying Obama’s reform plan

Banks and other firms are quick to attack Obama's consumer-friendly overhaul of financial rules. The stage is set for a legislative battle, with Wall Street turning to allies in Congress.

Average mortgage rates across the board fell in the week ending June 18 after spiking briefly the week before, according to a survey released today by mortgage giant Freddie Mac (FRE: 0.7353 +2.12%).

“Reports of benign inflation figures reversed the upward trend of mortgage rates this week,” however, “it’s still too early to tell whether the decline in housing market activity has hit bottom yet,” says Frank Nothaft, Freddie’s chief economist, in a media statement today.

Thirty-year fixed mortgages (FRMs) averaged 5.38% rates with an average 0.7 point, down from 5.59% last week. The average rate for a 15-year FRM came in at 4.89% with an average 0.7 point, from 5.06% last week. Five-year adjustable-rate mortgages (ARMs) averaged 4.97% with an average 0.6 point, from 5.17% last week, while one-year ARMs averaged 4.95% with an average 0.6 point, from 5.19% the week before.

A separate survey conducted by Bankrate.com confirmed a drop in rates, with 30-year FRMs averaging 5.76% with an average 0.43 point, down from 5.96% the previous week. Bankrate’s data also found 15-year FRMs down to 5.19% from 5.37%.

“The concerns about eventual inflation that drove bond yields and mortgage rates higher have been tempered by the reality of continued weakness in the economy,” Bankrate said in a media statement.

To read the original article click here

Additional articles of interest...

Originate to Distribute Mortgages Default More

Mortgages sold on the secondary market quickly after being originated were underwritten more poorly than loans kept on bank’s books, according to a report from the University of Michigan Ross School of Business.

We’ve Gone From Saving Wall Street in Order to Save Main Street to Just Saving Wall Street

But parsing through his 85-page plan, it's not clear how these reforms will ensure that our financial system works for the economy as a whole.

Wall Street isn’t buying Obama’s reform plan

Banks and other firms are quick to attack Obama's consumer-friendly overhaul of financial rules. The stage is set for a legislative battle, with Wall Street turning to allies in Congress.

Thursday, June 18, 2009

Too Big to Fail, or Succeed

Everyone will want to become big enough to enjoy 'systemic risk' protection. By Peter J. Wallison

In a speech at the White House yesterday, President Barack Obama outlined what he envisions for future regulation of the financial system. He called his plan "a new foundation for sustained economic growth . . . a transformation on a scale not seen since the reforms that followed the Great Depression." Indeed it is.

His plan, if adopted, will fundamentally change the nature of our financial system and economy. The underlying concerns and assumptions are clear, and they are made clearer by considering other ways that his administration has dealt with the consequences of competition -- particularly the faux bankruptcies of General Motors and Chrysler and the impending change in antitrust policy. Although the president said in his speech that he supports free markets, these initiatives confirm that the administration fears the "creative destruction" that free markets produce, preferring stability over innovation, competition and change.

To read original article click here

Other Articles of Interest...

The total number of people on the unemployment insurance rolls has dropped for the first time since early January, while first-time claims for benefits rose slightly, the Labor Department said Thursday.

Mortgage brokers will be obligated to sell the best available mortgage loans to avoid conflicts of interest between themselves and borrowers, while also determining the mortgages they sell are affordable to borrowers.

U.S. stocks snapped a three-day losing streak as reports on jobless claims and manufacturing added to evidence the recession may be near a bottom.

Subscribe to:

Comments (Atom)