Last month, 73.4 percent of Las Vegas-area homes and condos that were resold had been previously foreclosed on in the prior 12 months, according to DataQuick.

That’s up from the 55.9 percent share that was distressed a year earlier, a sign that the crisis is far from over.

The only good news (if you want to call it that), is that sales are up, with 4,536 new and resale homes and condos closing escrow during the month, up 1.9 percent from April and 23 percent from a year ago.

To view original article click here

Other good articles...

JPMorgan Tightens Grip on Equity Sales by Selling Own Shares

...helped by the sale of shares of financial firms, including their own.

Paper Avalanche Buries Plan to Stem Foreclosures

Think of the documents as being part of a pile massing inside the bank

Recovery threatened by toxic assets still hidden in key banks

Governments too slow to act, warn

Toxic Assets (PPIP) Death Rattle

Remember, folks, that the DOW surged by more than 500 points, a 7% gain, on the day the PPIP was announced.

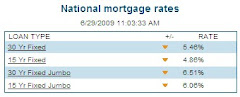

Monday, June 29, 2009

Friday, June 26, 2009

JPMorgan, Citigroup Expand in ‘Jumbo’ Loans for Expensive Homes

June 26 (Bloomberg) -- JPMorgan Chase & Co. and Citigroup Inc. are expanding in “jumbo” mortgages used to buy the most expensive homes, helping revive a market that shriveled amid a three-year jump in homeowner defaults.

JPMorgan resumed buying new jumbo loans made by other lenders this month, after halting purchases in March, spokesman Tom Kelly said. Borrowers must have checking accounts with the bank, he said. Citigroup is again offering the loans through independent mortgage brokers, spokesman Mark Rodgers said.

The two New York-based banks are signaling new interest in a market hobbled since 2007, when record-breaking defaults on home loans caused investors to flee securities backed by mortgages. With the recession sapping demand for new consumer and corporate loans, lenders are competing harder for creditworthy customers, said Harry Davis, banking professor at Appalachian State University in Boone, North Carolina.

“They have surely across the board raised lending standards, and there aren’t a lot of good borrowers standing in the lobby,” Davis said in an interview.

To read the original article click here

Other interesting articles...

Loan Modifications Up at Fannie, Freddie, But So Are Late Payments

Loan modifications at Fannie Mae and Freddie Mac were up 57 percent in the first quarter

41 Charges as Mortgage Fraud Hits Condos & Suburbs

Federal law enforcement officials recently announced charges have brought against 41 defendants in five separate cases in Chicago.

REQUIRED READING: The Fannie And Freddie Quandary

It's a perfect time to think about the fundamental restructuring of the world famous (and now broke) government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac.

Rep. Issa Says Fed ‘Engaged in a Cover-Up’ on Merrill-Bofa

U.S. Congressman Darrell Issa said the Federal Reserve “engaged in a cover-up”

JPMorgan resumed buying new jumbo loans made by other lenders this month, after halting purchases in March, spokesman Tom Kelly said. Borrowers must have checking accounts with the bank, he said. Citigroup is again offering the loans through independent mortgage brokers, spokesman Mark Rodgers said.

The two New York-based banks are signaling new interest in a market hobbled since 2007, when record-breaking defaults on home loans caused investors to flee securities backed by mortgages. With the recession sapping demand for new consumer and corporate loans, lenders are competing harder for creditworthy customers, said Harry Davis, banking professor at Appalachian State University in Boone, North Carolina.

“They have surely across the board raised lending standards, and there aren’t a lot of good borrowers standing in the lobby,” Davis said in an interview.

To read the original article click here

Other interesting articles...

Loan Modifications Up at Fannie, Freddie, But So Are Late Payments

Loan modifications at Fannie Mae and Freddie Mac were up 57 percent in the first quarter

41 Charges as Mortgage Fraud Hits Condos & Suburbs

Federal law enforcement officials recently announced charges have brought against 41 defendants in five separate cases in Chicago.

REQUIRED READING: The Fannie And Freddie Quandary

It's a perfect time to think about the fundamental restructuring of the world famous (and now broke) government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac.

Rep. Issa Says Fed ‘Engaged in a Cover-Up’ on Merrill-Bofa

U.S. Congressman Darrell Issa said the Federal Reserve “engaged in a cover-up”

Wednesday, June 24, 2009

Not Paying the Mortgage, Yet Stuck With the Keys

Foreclosure Backlog Imperils Recovery

A growing number of American homeowners are falling into financial limbo: They're badly behind on payments, but their banks have not yet foreclosed.

The backlog of seriously delinquent mortgages, which so far affects about 1 million borrowers, is a shadow over hopes for a rebound in the nation's housing markets. It masks the full extent of the foreclosure crisis and threatens to depress prices even further just as some parts of the country are hinting at recovery. For lenders, it could portend even more financial losses tied to the mortgage meltdown.

"It just means foreclosure rates are going to keep rising," said Patrick Newport, an economist for IHS Global Insight.

Rising mortgage delinquencies were at the root of the recession, and many economists say an economic recovery will be difficult until the housing market recovers and home prices stabilize.

And even though a delayed foreclosure can be a blessing for some troubled homeowners, for others, it simply prolongs the financial distress, leaving them on the hook for the condition of the property. Even if they move out, they cannot move on.

To read the entire article click here

Other interesting articles...

Citigroup Halts Some Mortgage Applications, Cites Missing

DataCitigroup Inc. suspended loan applications at a unit that produced half of its $115 billion in mortgages last year

Banks Oppose Financial Agency; Consumers Seek Clarity

U.S. bankers lined up against a new federal oversight agency proposed by President Barack Obama,

A growing number of American homeowners are falling into financial limbo: They're badly behind on payments, but their banks have not yet foreclosed.

The backlog of seriously delinquent mortgages, which so far affects about 1 million borrowers, is a shadow over hopes for a rebound in the nation's housing markets. It masks the full extent of the foreclosure crisis and threatens to depress prices even further just as some parts of the country are hinting at recovery. For lenders, it could portend even more financial losses tied to the mortgage meltdown.

"It just means foreclosure rates are going to keep rising," said Patrick Newport, an economist for IHS Global Insight.

Rising mortgage delinquencies were at the root of the recession, and many economists say an economic recovery will be difficult until the housing market recovers and home prices stabilize.

And even though a delayed foreclosure can be a blessing for some troubled homeowners, for others, it simply prolongs the financial distress, leaving them on the hook for the condition of the property. Even if they move out, they cannot move on.

To read the entire article click here

Other interesting articles...

Citigroup Halts Some Mortgage Applications, Cites Missing

DataCitigroup Inc. suspended loan applications at a unit that produced half of its $115 billion in mortgages last year

Banks Oppose Financial Agency; Consumers Seek Clarity

U.S. bankers lined up against a new federal oversight agency proposed by President Barack Obama,

Tuesday, June 23, 2009

May existing home sales rose 2.4 percent

Existing home sales rose 2.4 percent in May; prices plunge 16.8 percent

By Alan Zibel, AP Real Estate Writer

On Tuesday June 23, 2009, 10:40 am EDT

WASHINGTON (AP) -- Sales of previously occupied homes rose modestly from April to May, the third monthly increase this year, but signs of a housing recovery are fragile at best. The National Association of Realtors said Tuesday that home sales rose 2.4 percent last month to a seasonally adjusted annual rate of 4.77 million, from a downwardly revised pace of 4.66 million in April.

About one out of every three homes sold was a foreclosure or distressed sale. That helped drag down the median price to $173,000 -- 16.8 percent below a year ago.

Falling prices coupled with new rules for property appraisers have caused many transactions to fall apart or be delayed.

"We have just been flooded with e-mails, telephone calls on the appraisal problems," said Lawrence Yun, the Realtors' chief economist.

To read the original article click here

You may also want to read...

S&P Downgrades More U.S. Prime Jumbo RMBS

Economic Crisis Stirs Free-Market Debate

U.S. Economy: Slide in Home Prices Spurs Increase in Resales

By Alan Zibel, AP Real Estate Writer

On Tuesday June 23, 2009, 10:40 am EDT

WASHINGTON (AP) -- Sales of previously occupied homes rose modestly from April to May, the third monthly increase this year, but signs of a housing recovery are fragile at best. The National Association of Realtors said Tuesday that home sales rose 2.4 percent last month to a seasonally adjusted annual rate of 4.77 million, from a downwardly revised pace of 4.66 million in April.

About one out of every three homes sold was a foreclosure or distressed sale. That helped drag down the median price to $173,000 -- 16.8 percent below a year ago.

Falling prices coupled with new rules for property appraisers have caused many transactions to fall apart or be delayed.

"We have just been flooded with e-mails, telephone calls on the appraisal problems," said Lawrence Yun, the Realtors' chief economist.

To read the original article click here

You may also want to read...

S&P Downgrades More U.S. Prime Jumbo RMBS

Economic Crisis Stirs Free-Market Debate

U.S. Economy: Slide in Home Prices Spurs Increase in Resales

Monday, June 22, 2009

Fed plans repo markets revamp

By Henny Sender and Michael Mackenzie in New York

Published: June 21 2009 22:31 Last updated: June 21 2009 22:31

The US Federal Reserve is considering dramatic changes to the giant repurchase – or repo – markets where banks around the world raise overnight dollar loans.

The plans include creating a utility to replace the Wall Street banks that handle transactions, people familiar with the matter say.

The Fed’s deliberations are partly motivated by concerns that the structure of the US overnight repurchase market may have exacerbated the financial turmoil that accompanied the failure of Lehman Brothers in September last year.

Fed officials plan to meet next month with market participants to discuss reforms.

People familiar with the Fed’s thinking say it is looking into the creation of a mechanism to replace the clearing banks – the biggest of which are JPMorgan Chase and Bank of New York Mellon – that serve as intermediaries between borrowers and lenders.

“The Fed is raising questions about whether the system really protects the interests of all participants,” says one person familiar with the Fed’s thinking.

In the repo markets, borrowers, such as banks, pledge collateral in return for overnight loans from lenders, such as money market funds.

To read the original article click here

You may also want to read...

Making Home Affordable program may help more underwater homeowners

The Making Home Affordable program may be further expanded to help more underwater homeowners refinance their mortgages.

FHA warns it may need assistance top operate

The FHA continues to be overwhelmed by surging loan volume, as evidenced by remarks from Kenneth M. Donohue, Inspector General of HUD.

No recovery for U.S. property markets until 2017

The U.S. urban commercial real estate markets probably will not recover until 2017

Fed meeting gets underway

The Federal Open Market Committee begins a two-day meeting on interest rate policy.

Published: June 21 2009 22:31 Last updated: June 21 2009 22:31

The US Federal Reserve is considering dramatic changes to the giant repurchase – or repo – markets where banks around the world raise overnight dollar loans.

The plans include creating a utility to replace the Wall Street banks that handle transactions, people familiar with the matter say.

The Fed’s deliberations are partly motivated by concerns that the structure of the US overnight repurchase market may have exacerbated the financial turmoil that accompanied the failure of Lehman Brothers in September last year.

Fed officials plan to meet next month with market participants to discuss reforms.

People familiar with the Fed’s thinking say it is looking into the creation of a mechanism to replace the clearing banks – the biggest of which are JPMorgan Chase and Bank of New York Mellon – that serve as intermediaries between borrowers and lenders.

“The Fed is raising questions about whether the system really protects the interests of all participants,” says one person familiar with the Fed’s thinking.

In the repo markets, borrowers, such as banks, pledge collateral in return for overnight loans from lenders, such as money market funds.

To read the original article click here

You may also want to read...

Making Home Affordable program may help more underwater homeowners

The Making Home Affordable program may be further expanded to help more underwater homeowners refinance their mortgages.

FHA warns it may need assistance top operate

The FHA continues to be overwhelmed by surging loan volume, as evidenced by remarks from Kenneth M. Donohue, Inspector General of HUD.

No recovery for U.S. property markets until 2017

The U.S. urban commercial real estate markets probably will not recover until 2017

Fed meeting gets underway

The Federal Open Market Committee begins a two-day meeting on interest rate policy.

Friday, June 19, 2009

Rates Fall Back on Lower Inflation

By DIANA GOLOBAY June 18, 2009 10:39 AM CST

Average mortgage rates across the board fell in the week ending June 18 after spiking briefly the week before, according to a survey released today by mortgage giant Freddie Mac (FRE: 0.7353 +2.12%).

“Reports of benign inflation figures reversed the upward trend of mortgage rates this week,” however, “it’s still too early to tell whether the decline in housing market activity has hit bottom yet,” says Frank Nothaft, Freddie’s chief economist, in a media statement today.

Thirty-year fixed mortgages (FRMs) averaged 5.38% rates with an average 0.7 point, down from 5.59% last week. The average rate for a 15-year FRM came in at 4.89% with an average 0.7 point, from 5.06% last week. Five-year adjustable-rate mortgages (ARMs) averaged 4.97% with an average 0.6 point, from 5.17% last week, while one-year ARMs averaged 4.95% with an average 0.6 point, from 5.19% the week before.

A separate survey conducted by Bankrate.com confirmed a drop in rates, with 30-year FRMs averaging 5.76% with an average 0.43 point, down from 5.96% the previous week. Bankrate’s data also found 15-year FRMs down to 5.19% from 5.37%.

“The concerns about eventual inflation that drove bond yields and mortgage rates higher have been tempered by the reality of continued weakness in the economy,” Bankrate said in a media statement.

To read the original article click here

Additional articles of interest...

Originate to Distribute Mortgages Default More

Mortgages sold on the secondary market quickly after being originated were underwritten more poorly than loans kept on bank’s books, according to a report from the University of Michigan Ross School of Business.

We’ve Gone From Saving Wall Street in Order to Save Main Street to Just Saving Wall Street

But parsing through his 85-page plan, it's not clear how these reforms will ensure that our financial system works for the economy as a whole.

Wall Street isn’t buying Obama’s reform plan

Banks and other firms are quick to attack Obama's consumer-friendly overhaul of financial rules. The stage is set for a legislative battle, with Wall Street turning to allies in Congress.

Average mortgage rates across the board fell in the week ending June 18 after spiking briefly the week before, according to a survey released today by mortgage giant Freddie Mac (FRE: 0.7353 +2.12%).

“Reports of benign inflation figures reversed the upward trend of mortgage rates this week,” however, “it’s still too early to tell whether the decline in housing market activity has hit bottom yet,” says Frank Nothaft, Freddie’s chief economist, in a media statement today.

Thirty-year fixed mortgages (FRMs) averaged 5.38% rates with an average 0.7 point, down from 5.59% last week. The average rate for a 15-year FRM came in at 4.89% with an average 0.7 point, from 5.06% last week. Five-year adjustable-rate mortgages (ARMs) averaged 4.97% with an average 0.6 point, from 5.17% last week, while one-year ARMs averaged 4.95% with an average 0.6 point, from 5.19% the week before.

A separate survey conducted by Bankrate.com confirmed a drop in rates, with 30-year FRMs averaging 5.76% with an average 0.43 point, down from 5.96% the previous week. Bankrate’s data also found 15-year FRMs down to 5.19% from 5.37%.

“The concerns about eventual inflation that drove bond yields and mortgage rates higher have been tempered by the reality of continued weakness in the economy,” Bankrate said in a media statement.

To read the original article click here

Additional articles of interest...

Originate to Distribute Mortgages Default More

Mortgages sold on the secondary market quickly after being originated were underwritten more poorly than loans kept on bank’s books, according to a report from the University of Michigan Ross School of Business.

We’ve Gone From Saving Wall Street in Order to Save Main Street to Just Saving Wall Street

But parsing through his 85-page plan, it's not clear how these reforms will ensure that our financial system works for the economy as a whole.

Wall Street isn’t buying Obama’s reform plan

Banks and other firms are quick to attack Obama's consumer-friendly overhaul of financial rules. The stage is set for a legislative battle, with Wall Street turning to allies in Congress.

Thursday, June 18, 2009

Too Big to Fail, or Succeed

Everyone will want to become big enough to enjoy 'systemic risk' protection. By Peter J. Wallison

In a speech at the White House yesterday, President Barack Obama outlined what he envisions for future regulation of the financial system. He called his plan "a new foundation for sustained economic growth . . . a transformation on a scale not seen since the reforms that followed the Great Depression." Indeed it is.

His plan, if adopted, will fundamentally change the nature of our financial system and economy. The underlying concerns and assumptions are clear, and they are made clearer by considering other ways that his administration has dealt with the consequences of competition -- particularly the faux bankruptcies of General Motors and Chrysler and the impending change in antitrust policy. Although the president said in his speech that he supports free markets, these initiatives confirm that the administration fears the "creative destruction" that free markets produce, preferring stability over innovation, competition and change.

To read original article click here

Other Articles of Interest...

The total number of people on the unemployment insurance rolls has dropped for the first time since early January, while first-time claims for benefits rose slightly, the Labor Department said Thursday.

Mortgage brokers will be obligated to sell the best available mortgage loans to avoid conflicts of interest between themselves and borrowers, while also determining the mortgages they sell are affordable to borrowers.

U.S. stocks snapped a three-day losing streak as reports on jobless claims and manufacturing added to evidence the recession may be near a bottom.

Wednesday, June 17, 2009

Bill Calls for $15,000 Any-Time Home Buyer Credit

The Mortgage Bankers Association (MBA) on Monday declared its support for a Senate bill, S 1230 or the Homebuyer Tax Credit Act of 2009, which expands the current first-time home buyer tax credit from $8,000 to $15,000.

The bill also makes the tax credit available to anyone who purchases a principal residence in the year following the enactment of the bill. The MBA is already calling for monetization of the credit at the closing table on the grounds that more consumers will become home buyers if they don’t have to struggle to put away a substantial down payment.

You many also find interesting...

Monday, June 15, 2009

IMF Chief: Worst of Global Crisis Not Yet Over

ASTANA--The worst of the global economic crisis is not yet over but there are signs that the world has started to crawl out of recession, International Monetary Fund chief Dominique Strauss-Kahn said on Monday.

Finance ministers of the Group of Eight nations agreed over the weekend that the global economy was showing encouraging signs of stabilisation and started to consider how to unwind rescue steps for their economies.

The IMF managing director said on a visit to Kazakhstan that he largely agreed with their position but he appealed for caution in assessing the state of the global economy.

"Their (G8) stance is that we are beginning to see some green shoots but nevertheless we have to be cautious ... The large part of the worst is not yet behind us," he said in opening remarks at talks with Kazakh Prime Minister Karim Masimov.

"We see, at the IMF, a recovery towards the beginning of 2010. 2009 is already done, we know it's a bad year," he added.

"At the global economic level, the growth will be -1.3 (percent) which is the first negative growth since the Depression.

2010 may be better and we expect recovery in the first half of 2010."

To read the original article click here

Other articles of interest...

Oil falls below $72 as US dollar strengthens

"Oil is still very strong given the weak overall fundamentals,"

Stay the Course

The debate over economic policy has taken a predictable yet ominous turn

Obama Financial Reforms Outlined in Op-ed Piece

Senior Obama administration officials Monday said in a newspaper op-ed piece that a landmark financial regulation reform plan to be released this week…

Finance ministers of the Group of Eight nations agreed over the weekend that the global economy was showing encouraging signs of stabilisation and started to consider how to unwind rescue steps for their economies.

The IMF managing director said on a visit to Kazakhstan that he largely agreed with their position but he appealed for caution in assessing the state of the global economy.

"Their (G8) stance is that we are beginning to see some green shoots but nevertheless we have to be cautious ... The large part of the worst is not yet behind us," he said in opening remarks at talks with Kazakh Prime Minister Karim Masimov.

"We see, at the IMF, a recovery towards the beginning of 2010. 2009 is already done, we know it's a bad year," he added.

"At the global economic level, the growth will be -1.3 (percent) which is the first negative growth since the Depression.

2010 may be better and we expect recovery in the first half of 2010."

To read the original article click here

Other articles of interest...

Oil falls below $72 as US dollar strengthens

"Oil is still very strong given the weak overall fundamentals,"

Stay the Course

The debate over economic policy has taken a predictable yet ominous turn

Obama Financial Reforms Outlined in Op-ed Piece

Senior Obama administration officials Monday said in a newspaper op-ed piece that a landmark financial regulation reform plan to be released this week…

Friday, June 12, 2009

Citigroup Bailout Pays Taxpayers Three Times as Much as S&P 500

June 12 (Bloomberg) -- U.S. taxpayers have reaped a 7.5 percent return on the $45 billion used to rescue Citigroup Inc., more than three times as much as if the money had been invested in the Standard & Poor’s 500 Index.

Chief Executive Officer Vikram Pandit, summoned by Congress in February to explain his bank’s use of the funds, vowed to “make this a profitable investment for the American people.” The return since the government first purchased a stake in the bank on Oct. 28, which includes dividends, compares with 2.4 percent for the S&P 500 on that basis.

To read the entire article click here

Topics of interest...

Chief Executive Officer Vikram Pandit, summoned by Congress in February to explain his bank’s use of the funds, vowed to “make this a profitable investment for the American people.” The return since the government first purchased a stake in the bank on Oct. 28, which includes dividends, compares with 2.4 percent for the S&P 500 on that basis.

To read the entire article click here

Topics of interest...

Obama himself has said little about specific proposals

Economists are worried at the sharp rise in home mortgage rates over the past couple of weeks.

U.S. consumers' mood strongest in 9 months

U.S. consumer confidence rose to a nine-month high in June…

U.S. consumer confidence rose to a nine-month high in June…

Feeling Poorer? U.S. Household Wealth Shrivels

American households lost $1.33 trillion of their wealth in the first three months of the year…

American households lost $1.33 trillion of their wealth in the first three months of the year…

Thursday, June 11, 2009

One million option arms to reset in next four years??

An estimated one million option arms are expected to reset higher over the next four years, according to a Bloomberg report.

About three quarters of these loans will adjust next year and in 2011, with resets peaking in August 2011 when 54,000 loans are set to lose their negative amortization feature.

More than $750 billion in option arms were originated between 2004 and 2008, with hard-hit California accounting for roughly 58 percent of them.

One borrower cited in the Bloomberg report received one of the most toxic option arms I’ve never heard of, with a start rate of just 0.375 percent and a negative amortization ceiling of 145 percent.

That particular borrower will experience massive payment shock, with the monthly mortgage payment rising to $3,500 from just $98.

Click here to read the entire article

About three quarters of these loans will adjust next year and in 2011, with resets peaking in August 2011 when 54,000 loans are set to lose their negative amortization feature.

More than $750 billion in option arms were originated between 2004 and 2008, with hard-hit California accounting for roughly 58 percent of them.

One borrower cited in the Bloomberg report received one of the most toxic option arms I’ve never heard of, with a start rate of just 0.375 percent and a negative amortization ceiling of 145 percent.

That particular borrower will experience massive payment shock, with the monthly mortgage payment rising to $3,500 from just $98.

Click here to read the entire article

FTC Testifies on Efforts to Combat Foreclosure Rescue and Loan Modification Scams

Is this as big of a problem as they would like for us to believe?? To identify only eleven in over a years time frame doesn’t seem to warrant an “intensified” effort to me. What do you think?

The Federal Trade Commission today told the U.S. House Subcommittee on Housing and Community Opportunity of the Committee on Financial Services that, with the rapid increase in mortgage delinquencies and foreclosures, the FTC has intensified its efforts to protect consumers from foreclosure rescue and loan modification scams. The FTC also recommended legislative and other remedies to enhance the agency’s effectiveness.

Read more here…

The Federal Trade Commission today told the U.S. House Subcommittee on Housing and Community Opportunity of the Committee on Financial Services that, with the rapid increase in mortgage delinquencies and foreclosures, the FTC has intensified its efforts to protect consumers from foreclosure rescue and loan modification scams. The FTC also recommended legislative and other remedies to enhance the agency’s effectiveness.

Read more here…

Wednesday, June 10, 2009

Stocks fall ahead of gov't report card on banks

Stocks slip ahead of decision on which banks can repay bailout funds; European markets drop

Stephen Bernard, AP Business Writer

On Monday June 8, 2009, 9:58 am EDT

NEW YORK (AP) -- Investors turned away from stocks ahead of the latest government report card on banks.

Stocks fell Monday, sending the Dow Jones industrial average down by about 100 points. Overseas markets also pulled back.

The government is expected to announce as early as Monday which banks will be allowed to return bailout funds. JPMorgan Chase & Co., Goldman Sachs Group Inc. and American Express Co. are expected to get approval to repay their loans, according to The Washington Post.

Other banks that were told by the government last month to raise funds to help protect against a potential worsening in the economy must submit plans Monday about how they are raising that capital.

Investors are also booking some gains from the market's three-month rally as concerns linger about the economy. The Standard & Poor's 500 index has surged 39 percent from a 12-year low on March 9. Interest rates on government bonds are higher and oil prices are near six-month highs.

To read the entire story click here

Stephen Bernard, AP Business Writer

On Monday June 8, 2009, 9:58 am EDT

NEW YORK (AP) -- Investors turned away from stocks ahead of the latest government report card on banks.

Stocks fell Monday, sending the Dow Jones industrial average down by about 100 points. Overseas markets also pulled back.

The government is expected to announce as early as Monday which banks will be allowed to return bailout funds. JPMorgan Chase & Co., Goldman Sachs Group Inc. and American Express Co. are expected to get approval to repay their loans, according to The Washington Post.

Other banks that were told by the government last month to raise funds to help protect against a potential worsening in the economy must submit plans Monday about how they are raising that capital.

Investors are also booking some gains from the market's three-month rally as concerns linger about the economy. The Standard & Poor's 500 index has surged 39 percent from a 12-year low on March 9. Interest rates on government bonds are higher and oil prices are near six-month highs.

To read the entire story click here

Monday, June 8, 2009

Supreme Court asked to block Chrysler sale to Fiat pending appeal

Mark Sherman, Associated Press Writer

On Sunday June 7, 2009, 9:56 am EDT

WASHINGTON (AP) -- Three Indiana state pension and construction funds want the Supreme Court to block Chrysler's sale to Fiat so they can pursue an appeal in hopes of getting a better deal.

The funds filed emergency papers at the high court early Sunday.

An appeals court in New York approved the sale Friday, but gave objectors until Monday afternoon to try to get the Supreme Court to intervene. Chrysler LLC wants to sell the bulk of its assets to a group led by Italy's Fiat Group SpA as part of its plan to emerge from bankruptcy protection.

To read the entire article click here

On Sunday June 7, 2009, 9:56 am EDT

WASHINGTON (AP) -- Three Indiana state pension and construction funds want the Supreme Court to block Chrysler's sale to Fiat so they can pursue an appeal in hopes of getting a better deal.

The funds filed emergency papers at the high court early Sunday.

An appeals court in New York approved the sale Friday, but gave objectors until Monday afternoon to try to get the Supreme Court to intervene. Chrysler LLC wants to sell the bulk of its assets to a group led by Italy's Fiat Group SpA as part of its plan to emerge from bankruptcy protection.

To read the entire article click here

Sunday, June 7, 2009

Fed damps hopes on mortgage-backed securities

By Aline van Duyn in New York

Published: June 4 2009 20:16 Last updated: June 4 2009 20:16

The US Federal Reserve on Thursday damped expectations that it was preparing to prop up the market for distressed bubble-era securities backed by mortgages.

Hopes that the Fed would in the coming months start providing financing to investors seeking to buy residential mortgage-backed securities (RMBS) – many of which have lost their triple A credit ratings – have pushed prices on these assets higher in recent months.

William Dudley, president of the Federal Reserve Bank of New York, said on Thursday that a decision had not been made. “We have not made a final decision on whether it is doable and, if it is doable, whether it is worth the cost,” he said.

Mr Dudley, who took over from Tim Geithner in January, has overseen the implementation of the $1,000bn term “asset-backed securities loan facility” (Talf), a key plank in the US government’s efforts to plug the hole left by the collapse of the asset-backed securities markets.

So far, the Talf has been used to finance the purchases of securities backed by loans to consumers, such as car and credit card loans. The Talf lends money to investors such as hedge funds on favorable terms, which encourages the purchases. This week, Talf financed 13 deals worth $16.4bn.

For the original article click here

Published: June 4 2009 20:16 Last updated: June 4 2009 20:16

The US Federal Reserve on Thursday damped expectations that it was preparing to prop up the market for distressed bubble-era securities backed by mortgages.

Hopes that the Fed would in the coming months start providing financing to investors seeking to buy residential mortgage-backed securities (RMBS) – many of which have lost their triple A credit ratings – have pushed prices on these assets higher in recent months.

William Dudley, president of the Federal Reserve Bank of New York, said on Thursday that a decision had not been made. “We have not made a final decision on whether it is doable and, if it is doable, whether it is worth the cost,” he said.

Mr Dudley, who took over from Tim Geithner in January, has overseen the implementation of the $1,000bn term “asset-backed securities loan facility” (Talf), a key plank in the US government’s efforts to plug the hole left by the collapse of the asset-backed securities markets.

So far, the Talf has been used to finance the purchases of securities backed by loans to consumers, such as car and credit card loans. The Talf lends money to investors such as hedge funds on favorable terms, which encourages the purchases. This week, Talf financed 13 deals worth $16.4bn.

For the original article click here

Saturday, June 6, 2009

FDIC Insurance Coverage

Extension of Temporary Increase in Standard Maximum Deposit Insurance Amount

President Obama has increased the insurance amount per depositor from $100,000 to $250,000. Can we afford that? Seems to me that the FDIC is taking quite a beating already. The increase is in effect until the end of 2013. Here’s the article:

Summary:

On May 20, 2009, President Barack Obama signed the Helping Families Save Their Homes Act, which extends the temporary increase in the standard maximum deposit insurance amount (SMDIA) to $250,000 per depositor through December 31, 2013. This extension of the temporary $250,000 coverage limit became effective immediately upon the President's signature. The legislation provides that the SMDIA will return to $100,000 on January 1, 2014.

Click here to read the entire article

President Obama has increased the insurance amount per depositor from $100,000 to $250,000. Can we afford that? Seems to me that the FDIC is taking quite a beating already. The increase is in effect until the end of 2013. Here’s the article:

Summary:

On May 20, 2009, President Barack Obama signed the Helping Families Save Their Homes Act, which extends the temporary increase in the standard maximum deposit insurance amount (SMDIA) to $250,000 per depositor through December 31, 2013. This extension of the temporary $250,000 coverage limit became effective immediately upon the President's signature. The legislation provides that the SMDIA will return to $100,000 on January 1, 2014.

Click here to read the entire article

Tuesday, June 2, 2009

Geithner tells China its dollar assets are safe

The students in China found our Timothy Geithner funny as he tries to convince them that their investment in our economy is safe...

Mon, 01 Jun 2009

From Reuters: Geithner tells China its dollar assets are safe “Chinese assets are very safe,” Geithner said in response to a question after a speech at Peking University, where he studied Chinese as a student in the 1980’s. His answer drew loud laughter from his student audience, reflecting skepticism in China about the wisdom of a developing….click here for the original story.

Mon, 01 Jun 2009

From Reuters: Geithner tells China its dollar assets are safe “Chinese assets are very safe,” Geithner said in response to a question after a speech at Peking University, where he studied Chinese as a student in the 1980’s. His answer drew loud laughter from his student audience, reflecting skepticism in China about the wisdom of a developing….click here for the original story.

Friday, May 29, 2009

Bair Attacks Too-Big-to-Fail as Enforcer Geithner Must Trust

I read an article on Bloomberg.com by Alison Vekshin about a meeting that Sheila Bair, chairman of the FCIC had with President Obama. She is not a proponent of the too big to fail idea.

“The FDIC head isn’t done expanding her influence over Wall Street. An opponent of the “too-big-to-fail” policy for firms like Citigroup Inc., Bair is lobbying Congress to give the FDIC authority to wind down bank and thrift holding companies -- a move she says is necessary to protect taxpayers. And she wants lawmakers to include the agency in a systemic risk council to prevent future financial shocks.”

To read the entire article click here.

“The FDIC head isn’t done expanding her influence over Wall Street. An opponent of the “too-big-to-fail” policy for firms like Citigroup Inc., Bair is lobbying Congress to give the FDIC authority to wind down bank and thrift holding companies -- a move she says is necessary to protect taxpayers. And she wants lawmakers to include the agency in a systemic risk council to prevent future financial shocks.”

To read the entire article click here.

Tuesday, May 26, 2009

Job Losses Push Safer Mortgages to Foreclosure

As job losses rise, growing numbers of American homeowners with once solid credit are falling behind on their mortgages, amplifying a wave of foreclosures.

In the latest phase of the nation’s real estate disaster, the locus of trouble has shifted from subprime loans — those extended to home buyers with troubled credit — to the far more numerous prime loans issued to those with decent financial histories.

To read the full story click here

In the latest phase of the nation’s real estate disaster, the locus of trouble has shifted from subprime loans — those extended to home buyers with troubled credit — to the far more numerous prime loans issued to those with decent financial histories.

To read the full story click here

Thursday, May 21, 2009

Credit Reform

There are some changes being made on how credit card companies, Mastercard or Visa, approach college students and also some changes to how and when they can raise interest rates. It is designed to help consumers make more informed decisions on credit. Read the article below…

By ANNE FLAHERTY, Associated Press Writer Anne Flaherty, Associated Press Writer – Thu May 21, 5:54 am ET

WASHINGTON – It's an end of an era for the thousands of college students who rely on MasterCard or Visa to get them through tight times.

Under a new law awaiting President Barack Obama's signature, credit card companies will be prohibited from giving cards to people under 21 unless they can prove they have the means to repay the debt or a parent or guardian co-signs for the loan.

Congress passed the bill this week, and Obama was expected to sign it into law Friday. The changes will go into effect in nine months. "The hope is that when they spend, they'll spend under better terms and there'll be fewer traps for them," said Pedro de la Torre, a spokesman for Campus Progress, a progressive group in Washington that tracks issues affecting young people.

Congress is hoping to break a vicious cycle: A cardholder falls behind in paying the bill and watches helplessly as the interest rate spikes on the existing balance. Buried in higher rates and late fees, the cardholder spend less, which hurts local businesses.

To read the entire article click here

By ANNE FLAHERTY, Associated Press Writer Anne Flaherty, Associated Press Writer – Thu May 21, 5:54 am ET

WASHINGTON – It's an end of an era for the thousands of college students who rely on MasterCard or Visa to get them through tight times.

Under a new law awaiting President Barack Obama's signature, credit card companies will be prohibited from giving cards to people under 21 unless they can prove they have the means to repay the debt or a parent or guardian co-signs for the loan.

Congress passed the bill this week, and Obama was expected to sign it into law Friday. The changes will go into effect in nine months. "The hope is that when they spend, they'll spend under better terms and there'll be fewer traps for them," said Pedro de la Torre, a spokesman for Campus Progress, a progressive group in Washington that tracks issues affecting young people.

Congress is hoping to break a vicious cycle: A cardholder falls behind in paying the bill and watches helplessly as the interest rate spikes on the existing balance. Buried in higher rates and late fees, the cardholder spend less, which hurts local businesses.

To read the entire article click here

Monday, May 18, 2009

FED UP

Commentary

Fed Up

Ron Paul, 05.15.09, 07:10 PM EDT

Audit the Federal Reserve.

(found at forbes.com)

The Federal Reserve's recent and unprecedented actions in the realm of monetary policy have provoked a backlash among the American people. Trillions of dollars worth of loans and guarantees have been provided to Wall Street firms, while Main Street Americans suffocate under harsh taxation, the prospect of higher debt levels and increasing inflation. These events have awakened many Americans to problems with the Fed's loose monetary policy, the bubbles it has created in the past and the potential hyperinflation it might cause in the future.

One of the fallacies of modern economics is the idea that a central bank is required in order to keep inflation low and promote economic growth. In reality, it is the central bank's monetary policy that causes inflation and depresses economic growth. Inflation is an increase in the supply of money, which in our day and age is directly caused or initiated by central banks. All other things being equal, inflation results in a rise in prices. A so-called "mild" rate of inflation of 3% per year leads to a 56% rise in prices over a 15-year period. Even a "low" rate of inflation of 2% per year leads to a 35% rise over that same period. How is that conducive to long-term growth?

read more on this article

Fed Up

Ron Paul, 05.15.09, 07:10 PM EDT

Audit the Federal Reserve.

(found at forbes.com)

The Federal Reserve's recent and unprecedented actions in the realm of monetary policy have provoked a backlash among the American people. Trillions of dollars worth of loans and guarantees have been provided to Wall Street firms, while Main Street Americans suffocate under harsh taxation, the prospect of higher debt levels and increasing inflation. These events have awakened many Americans to problems with the Fed's loose monetary policy, the bubbles it has created in the past and the potential hyperinflation it might cause in the future.

One of the fallacies of modern economics is the idea that a central bank is required in order to keep inflation low and promote economic growth. In reality, it is the central bank's monetary policy that causes inflation and depresses economic growth. Inflation is an increase in the supply of money, which in our day and age is directly caused or initiated by central banks. All other things being equal, inflation results in a rise in prices. A so-called "mild" rate of inflation of 3% per year leads to a 56% rise in prices over a 15-year period. Even a "low" rate of inflation of 2% per year leads to a 35% rise over that same period. How is that conducive to long-term growth?

read more on this article

Friday, May 15, 2009

Deals abound but buyers frustrated, columnist finds

By SHANNON BEHNKEN The Tampa Tribune

Published: May 15, 2009

Ray White thought now was the perfect time to help his daughter buy her first home.

Home prices are more affordable than they have been in years, interest rates are low, there are plenty of homes on the market, and the federal government is offering an $8,000 tax credit.

But because of one problem after another, every house they find seems out of her reach — even though she's approved for a loan and has a down payment.

"The other night, she just broke down and cried," White said, noting that they've looked at more than 100 homes. "I actually have this feeling right now that it's almost impossible for her to buy a house."

That's partly because the Whites are competing with investors who often pay cash and then flip the property for big profit. They typically won't sell to those getting an FHA loan, which are very popular among first-time homebuyers.

Read More…

Published: May 15, 2009

Ray White thought now was the perfect time to help his daughter buy her first home.

Home prices are more affordable than they have been in years, interest rates are low, there are plenty of homes on the market, and the federal government is offering an $8,000 tax credit.

But because of one problem after another, every house they find seems out of her reach — even though she's approved for a loan and has a down payment.

"The other night, she just broke down and cried," White said, noting that they've looked at more than 100 homes. "I actually have this feeling right now that it's almost impossible for her to buy a house."

That's partly because the Whites are competing with investors who often pay cash and then flip the property for big profit. They typically won't sell to those getting an FHA loan, which are very popular among first-time homebuyers.

Read More…

Tuesday, May 12, 2009

Goldman to Pay $60 Million in Subprime Settlement (Update1)

The loan modifications aren't over. Not by a long shot. Read this article by Kathleen M. Howley and Christine Harper

May 11 (Bloomberg) -- Goldman Sachs Group Inc. agreed to pay about $60 million to settle a Massachusetts investigation into the packaging of mortgage securities at the root of the collapse of the U.S. housing market.

The agreement calls for the bank to pay about $50 million to compensate homeowners and the rest to the state, Massachusetts Attorney General Martha Coakley said today at a news conference in Boston. The deal will also allow for some loan principal reductions. Goldman Sachs directly holds 714 Massachusetts mortgages, she said.

The bundling of the riskiest type of mortgages into securities turned the U.S. housing slump into a global recession as foreclosures deflated bond values and toppled Wall Street firms such as Lehman Brothers Holdings Inc. The Massachusetts attorney general has investigated Fremont Investment & Loan, now defunct, and H&R Block Inc., owner of Option One Mortgage Corp., for making the types of mortgages that Goldman securitized. Read more...

May 11 (Bloomberg) -- Goldman Sachs Group Inc. agreed to pay about $60 million to settle a Massachusetts investigation into the packaging of mortgage securities at the root of the collapse of the U.S. housing market.

The agreement calls for the bank to pay about $50 million to compensate homeowners and the rest to the state, Massachusetts Attorney General Martha Coakley said today at a news conference in Boston. The deal will also allow for some loan principal reductions. Goldman Sachs directly holds 714 Massachusetts mortgages, she said.

The bundling of the riskiest type of mortgages into securities turned the U.S. housing slump into a global recession as foreclosures deflated bond values and toppled Wall Street firms such as Lehman Brothers Holdings Inc. The Massachusetts attorney general has investigated Fremont Investment & Loan, now defunct, and H&R Block Inc., owner of Option One Mortgage Corp., for making the types of mortgages that Goldman securitized. Read more...

Friday, May 8, 2009

Geithner Bets U.S. Can Avoid Japan Trap Through Bank Earnings

By Rich Miller and Matthew Benjamin

May 8 (Bloomberg) -- Treasury Secretary Timothy Geithner is betting that U.S. banks can do something their Japanese counterparts were unable to accomplish in that country’s “lost decade” of the 1990s: earn their way out of trouble.

The stress-test results released yesterday by regulators found that the 19 largest banks face a $74.6 billion capital hole that may be filled mostly by private money. That compares with the hundreds of billions of dollars seen by outside analysts, including the International Monetary Fund, and takes into account banks’ projected earnings over the next two years.

Read more…

May 8 (Bloomberg) -- Treasury Secretary Timothy Geithner is betting that U.S. banks can do something their Japanese counterparts were unable to accomplish in that country’s “lost decade” of the 1990s: earn their way out of trouble.

The stress-test results released yesterday by regulators found that the 19 largest banks face a $74.6 billion capital hole that may be filled mostly by private money. That compares with the hundreds of billions of dollars seen by outside analysts, including the International Monetary Fund, and takes into account banks’ projected earnings over the next two years.

Read more…

Monday, May 4, 2009

Mortgage Fraud Epidemic: How the FBI Blew It and Why There's No 'Perp Walks'

Posted Apr 06, 2009 08:00am EDT by Aaron Task

In the wake of the bursting of the housing bubble, you'd think there'd be a significant number of investigations into criminal wrongdoing and accounting fraud, similar to what occurred after the S&L crisis and bursting of the stock bubble in 2000.

But two years into the crisis the FBI "doesn't have a single major conviction or indictment of anyone," notes William Black, a former senior bank regulator and S&L prosecutor, and currently an Associate Professor of Economics and Law at the University of Missouri - Kansas City.

Black, who was counsel to the Federal Home Loan Bank Board during the S&L crisis of the 1980s and blew the whistle on the "Keating Five" in 1989, reiterated what he told us in November: Though the FBI warned of an "epidemic" of mortgage fraud in 2004, they subsequently made a "strategic alliance" with the Mortgage Bankers Association, which Black calls the "trade association of perps."

Read more…

In the wake of the bursting of the housing bubble, you'd think there'd be a significant number of investigations into criminal wrongdoing and accounting fraud, similar to what occurred after the S&L crisis and bursting of the stock bubble in 2000.

But two years into the crisis the FBI "doesn't have a single major conviction or indictment of anyone," notes William Black, a former senior bank regulator and S&L prosecutor, and currently an Associate Professor of Economics and Law at the University of Missouri - Kansas City.

Black, who was counsel to the Federal Home Loan Bank Board during the S&L crisis of the 1980s and blew the whistle on the "Keating Five" in 1989, reiterated what he told us in November: Though the FBI warned of an "epidemic" of mortgage fraud in 2004, they subsequently made a "strategic alliance" with the Mortgage Bankers Association, which Black calls the "trade association of perps."

Read more…

Friday, March 20, 2009

Reverse Mortgages?

Can you think of one single reason to get into the reverse mortgage business? I can think of 78 million of them.

No joke, that’s the number of baby boomers heading toward retirement. Did you know that foreclosure and bankruptcy is up among the senior population? They are seeing their investments spiral downward right before their eyes and they have expenses that some of us don’t think about like medication and medical expenses.

Reverse Mortgage marketing is not media hype. It’s very real. Don’t let this market and the opportunity it presents pass you by. The Federal Housing Administration Home Equity Conversion Mortgage lending limit is set at $625,500 for 2009.

Why would seniors be interested in reverse mortgages? With Lenders tightening up their lending guidelines today there is no where else they can get a loan with no income, credit or asset verification. The qualification is based on the equity in their home and the age of the borrower. There are no payments due as long as the senior lives in the home and they can have a line of credit that cannot be frozen. That alone is unheard of today! Reverse Mortgages are backed by FHA and includes a non-recourse clause so their heirs can’t be held responsible for the debt once the home is sold.

There is a new Reverse Mortgage product coming out April 1st! Stay tuned…

No joke, that’s the number of baby boomers heading toward retirement. Did you know that foreclosure and bankruptcy is up among the senior population? They are seeing their investments spiral downward right before their eyes and they have expenses that some of us don’t think about like medication and medical expenses.

Reverse Mortgage marketing is not media hype. It’s very real. Don’t let this market and the opportunity it presents pass you by. The Federal Housing Administration Home Equity Conversion Mortgage lending limit is set at $625,500 for 2009.

Why would seniors be interested in reverse mortgages? With Lenders tightening up their lending guidelines today there is no where else they can get a loan with no income, credit or asset verification. The qualification is based on the equity in their home and the age of the borrower. There are no payments due as long as the senior lives in the home and they can have a line of credit that cannot be frozen. That alone is unheard of today! Reverse Mortgages are backed by FHA and includes a non-recourse clause so their heirs can’t be held responsible for the debt once the home is sold.

There is a new Reverse Mortgage product coming out April 1st! Stay tuned…

Friday, February 20, 2009

Could Mortgage Brokers Become Extinct?

With some large banks cutting back on doing business with mortgage brokers many mortgage brokers or mortgage companies could be closing their doors.

This could be very bad news for borrowers because with fewer brokers in the marketplace things will become less competitive and more expensive for you to obtain a home loan. It won’t be so easy to shop and compare rates.

To read the entire article, please visit: http://money.cnn.com/2009/02/12/real_estate/lenders_drop_mortgage_brokers/index.htm?postversion=2009021213

This could be very bad news for borrowers because with fewer brokers in the marketplace things will become less competitive and more expensive for you to obtain a home loan. It won’t be so easy to shop and compare rates.

To read the entire article, please visit: http://money.cnn.com/2009/02/12/real_estate/lenders_drop_mortgage_brokers/index.htm?postversion=2009021213

Monday, February 16, 2009

REVERSE MORTGAGES

It is thought that since the “baby boomers” are reaching retirement that there will be a huge demand for Reverse Mortgages. The baby boomer’s are generally referred to the baby’s that were born between 1946 and 1964.

In order to qualify for a RM (reverse mortgage) you must first own your home outright (or minimal balance), all owners must be at least 62 years of age and you must live in your home.

You should always consult with your family attorney or financial advisor before entering into a Reverse Mortgage. Your home is a valuable asset and knowing your rights and responsibilities as a borrower may help minimize any financial risks you may face.

The loan proceeds can be paid to you in monthly advances, through a line-of-credit, a lump sum payment or a combination of all three options. The amount that you can borrower generally is based on your age, the equity in your home and the interest rate the lender is offering. Sine you still own the home you will still be responsible for the taxes, repairs and maintenance.

You are protected under the Federal Truth in Lending Act (TILA), which requires your lender to inform you about the plan’s terms and costs. Be sure that you understand them before you sign anything. Lenders must provide specific information on rates and payment terms.

Key Point to Remember

Your legal obligation to pay back the loan is limited by the value of your home at the time you pay off the loan.

You can never owe more than the home is worth.

The loan proceeds are not taxable. If you receive Social Security Income the advances will not affect your benefits as long as you spend them within the month you receive them.

When in doubt, check with a benefits special at a local agency or legal services office.

A good source of information is AARP. You can write them at:

AARP Home Equity Information Center

601 E. Street, NW

Washington, DC 20049 or visit their website at http://www.aarp.org/

Tuesday, February 3, 2009

Forensic Loan Audit

It has been estimated that over 80% of loans that were obtained between 2001 and 2006 have predatory lending violations. Most of the violations involve TILA (Truth In Lending Act) or RESPA (Real Estate Settlement Protection Act). The Lender or Bank that now owns these loans is now liable for these violations. The penalties vary but in most cases the bank would be responsible to pay legal fees for both parties if they are found to be in violation. That can add up fast.

Any homeowner that is serious about obtaining an aggressive loan modification should start with a Forensic Loan Audit. There are many companies out there willing to do a forensic audit independent of a modification service or in conjunction with their loan modification services. This is not intended to be legal advice, (you will need to consult an attorney) but an experienced attorney can tell you exactly what the consequences are. If you do decide to proceed have your attorney request a restraining order so that no payments or late fees will be required until the situation has been resolved. With the threat of foreclosure and the possible litigation might be enough for your lender to reduce your balance to current market value as well as a possible rate reduction.

If you attempt to do the loan modification your self and don’t have success (remember to be persistent) it may be time to seek the services of an attorney to negotiate on your behalf. When you have an attorney requesting loan documents and fighting for your loan modification the bank is more likely to work with you. They will realize that the threat of being sued to real. You may determine that the $2,000 - $4,000 that you will spend for an attorney will be well worth it if your principal balance and interest rates are reduced.

Any homeowner that is serious about obtaining an aggressive loan modification should start with a Forensic Loan Audit. There are many companies out there willing to do a forensic audit independent of a modification service or in conjunction with their loan modification services. This is not intended to be legal advice, (you will need to consult an attorney) but an experienced attorney can tell you exactly what the consequences are. If you do decide to proceed have your attorney request a restraining order so that no payments or late fees will be required until the situation has been resolved. With the threat of foreclosure and the possible litigation might be enough for your lender to reduce your balance to current market value as well as a possible rate reduction.

If you attempt to do the loan modification your self and don’t have success (remember to be persistent) it may be time to seek the services of an attorney to negotiate on your behalf. When you have an attorney requesting loan documents and fighting for your loan modification the bank is more likely to work with you. They will realize that the threat of being sued to real. You may determine that the $2,000 - $4,000 that you will spend for an attorney will be well worth it if your principal balance and interest rates are reduced.

Friday, January 30, 2009

Basic Guide For A Loan Modification

Keep in mind that no two lenders are created equal; meaning their steps for modifications will vary. Here are some guidelines to reference.

1st – Don’t pay debt with debt. This will generally lead to bankruptcy. Do not hide from your lender. Communication is key.

2nd – Make a list of all of your outstanding debts. See where your money is going. Compare your debts to your income and see how much you have left over at the end of the month. If your debts are higher than your income you need to see where you have to cut back. Always start with all of your expenses and then cut back or adjust where you can. This will help when you contact your lender.

3rd - Contact your lender and ask for the loss mitigation department. Make sure they don’t’ direct you to the collections department. That is NOT who you want to speak to. Have them explain to you in detail exactly what they will need to consider your modification. You may be able to persuade them to freeze your loan. This means that won’t assess late fees, credit lates or start foreclosure proceedings until after the modification decision has been made. If you have suffered a hardship this would be the time discuss that. (Job loss, divorce, arm adjustment, etc)

4th – Once the loss mitigation reviews all of your documents and accepts your proposal you did a great job and it’s time to celebrate. Unfortunately it’s rarely that easy. Most times this is where the negotiations start. They wont’ deviate far from the actual numbers that you submitted. Your income, the value of the property and the loss they will take in foreclosure. If you have documented your case correctly you should come out of the negotiation with something you can afford.

5th – If they deny your request for loan modification then unfortunately its time to seek the advice of an attorney or an attorney based loan Modification Company. If you have not already examined your loan documents for TILA or RESPA violation then ask the attorney to research that. If one is found the bank will re-open your request. They would rather modify than be sued.

6th – The bank can’t modify your loan without your notarized signature. Be sure to read the modification agreement closely. Once your loan is modified and you place your signature on the new agreement it’s a done deal. There are no 2nd chances. You may want to have an attorney review the documents prior to signing.

Next post we’ll talk a little about a Forensic Loan Audit…

1st – Don’t pay debt with debt. This will generally lead to bankruptcy. Do not hide from your lender. Communication is key.

2nd – Make a list of all of your outstanding debts. See where your money is going. Compare your debts to your income and see how much you have left over at the end of the month. If your debts are higher than your income you need to see where you have to cut back. Always start with all of your expenses and then cut back or adjust where you can. This will help when you contact your lender.

3rd - Contact your lender and ask for the loss mitigation department. Make sure they don’t’ direct you to the collections department. That is NOT who you want to speak to. Have them explain to you in detail exactly what they will need to consider your modification. You may be able to persuade them to freeze your loan. This means that won’t assess late fees, credit lates or start foreclosure proceedings until after the modification decision has been made. If you have suffered a hardship this would be the time discuss that. (Job loss, divorce, arm adjustment, etc)

4th – Once the loss mitigation reviews all of your documents and accepts your proposal you did a great job and it’s time to celebrate. Unfortunately it’s rarely that easy. Most times this is where the negotiations start. They wont’ deviate far from the actual numbers that you submitted. Your income, the value of the property and the loss they will take in foreclosure. If you have documented your case correctly you should come out of the negotiation with something you can afford.

5th – If they deny your request for loan modification then unfortunately its time to seek the advice of an attorney or an attorney based loan Modification Company. If you have not already examined your loan documents for TILA or RESPA violation then ask the attorney to research that. If one is found the bank will re-open your request. They would rather modify than be sued.

6th – The bank can’t modify your loan without your notarized signature. Be sure to read the modification agreement closely. Once your loan is modified and you place your signature on the new agreement it’s a done deal. There are no 2nd chances. You may want to have an attorney review the documents prior to signing.

Next post we’ll talk a little about a Forensic Loan Audit…

Thursday, January 29, 2009

Where To Start

First, you need to find the number for the Loss Mitigation Department for your lender. Most lenders have this information posted on their websites but you can call the number on your statement and just ask.

Once you have requested assistance you will be a assigned an underwriter or a loss mitigation representative. This person will be very instrumental in helping you obtain a satisfactory modification so one of the most important bits of advice I can give you is, “BE BICE”. Remember that they are not the ones that got you into this situation and you are relying on them to help you get out of it. Even if it’s a situation where you don’t deal with just one person they will have detailed notes for all to read in their system so be nice to everyone you speak to.

Loss mitigation departments are quite busy these days so a little bit of understanding goes a long way, be patient. Don’t be afraid to be persistent but at the same time understanding. Call every day if necessary but listen carefully and don’t ignore their advice. Let them know how serious you are about modifying your loan. You just want to keep your home. Next post we’ll highlight the exact steps you should take…

Once you have requested assistance you will be a assigned an underwriter or a loss mitigation representative. This person will be very instrumental in helping you obtain a satisfactory modification so one of the most important bits of advice I can give you is, “BE BICE”. Remember that they are not the ones that got you into this situation and you are relying on them to help you get out of it. Even if it’s a situation where you don’t deal with just one person they will have detailed notes for all to read in their system so be nice to everyone you speak to.

Loss mitigation departments are quite busy these days so a little bit of understanding goes a long way, be patient. Don’t be afraid to be persistent but at the same time understanding. Call every day if necessary but listen carefully and don’t ignore their advice. Let them know how serious you are about modifying your loan. You just want to keep your home. Next post we’ll highlight the exact steps you should take…

Wednesday, January 28, 2009

Negotiating Your Modification

While a foreclosure is like watching your dream home being flushed down the toilet, it is also scary to the bank to think of the foreclosure process. Always remember, your modification is a negotiation. And hopefully, a negotiation that you and your bank can live with.

Always begin your negotiation with a rate lower than you think you can get. This way you have room to negotiate. When you are explaining to the Lender that when you give them a new estimated value for your property that you back it up. You can contact a local appraiser or realtor to see what the properties in your neighborhood are going for or you try some of these popular sites: www.zillow.com, www.cyberhomes.com, www.comps.com. If the value is less than what you owe then ask for a principal reduction. Note: One your loan is modified it’s a done deal. There will be no 2nd chances so be sure the terms are something that you can live with for as long as you plan to stay in the home.

Always begin your negotiation with a rate lower than you think you can get. This way you have room to negotiate. When you are explaining to the Lender that when you give them a new estimated value for your property that you back it up. You can contact a local appraiser or realtor to see what the properties in your neighborhood are going for or you try some of these popular sites: www.zillow.com, www.cyberhomes.com, www.comps.com. If the value is less than what you owe then ask for a principal reduction. Note: One your loan is modified it’s a done deal. There will be no 2nd chances so be sure the terms are something that you can live with for as long as you plan to stay in the home.

Friday, January 23, 2009

Most Common Loan Modifications - ARM's

The most common example of someone in need of a loan modification are those that are in soon to adjust ARM’s (adjustable rate mortgages) or even worse scenario is a POA (payment option arm a/k/a negative amortization). Your ARM is about to adjust to a higher interest rate causing your payment to increase $200 or more per month and you just can’t swing it. If you have suffered a job loss, divorce or your property value had dramatically decreased your chances of refinancing into a fixed rate are not very good if not impossible. With this type of hardship your only options are to lose your house or modify the loan. That is what the bank needs to understand. If you were making your payments on time with the payment you had before the rate adjustment the bank is likely to agree to the interest rate reduction or extending the length of your loan to 40 years or more with no problem.

Principal Balance Reductions

Principal balance reductions are not favorable to a bank and rarely do they offer this option. When they do decide to grant a reduction they do it only because the value of the property is much less than the balance you own and there would be no reason for you do anything other than walk away. An important note though is that if they grant a principal balance reduction the bank can issue you a 1009 for the forgiven amount. This is something that you will need to discuss with your tax attorney and decide if you should ask your bank to waive this. This article is in no way meant to be legal advice.

If you have a 1st and a 2nd mortgage your chances of a principal reduction is greater. That’s because in a foreclosure situation the bank holding the 2nd mortgage will likely get nothing. The bank would rather get 20 cents on the dollar than risk getting nothing. If the same bank owns both the 1st and the 2nd mortgages you are in the best possible scenario for a reduction. If they are owned by different banks then it things are a little more challenging. When a bank only owns the 2nd mortgage they will most likely to fight for whatever they can get. If your loans are owned by the same bank they will most likely be more concerned with getting the first into a manageable situation while viewing the 2nd as almost worthless.

Keep in mind that the banks DO NOT want to be in the real estate business. They don’t want to foreclose on a property in a declining market. In today’s market the banks stand to lose $0.35 to $0.80 on the dollar on any foreclosed property. If we were in a booming market the scenario would be more in the banks favor and you would most likely not be reading this post. Any bank would rather collect lower payments than none at all.

Next post we will discuss Negotiations…

Principal Balance Reductions

Principal balance reductions are not favorable to a bank and rarely do they offer this option. When they do decide to grant a reduction they do it only because the value of the property is much less than the balance you own and there would be no reason for you do anything other than walk away. An important note though is that if they grant a principal balance reduction the bank can issue you a 1009 for the forgiven amount. This is something that you will need to discuss with your tax attorney and decide if you should ask your bank to waive this. This article is in no way meant to be legal advice.

If you have a 1st and a 2nd mortgage your chances of a principal reduction is greater. That’s because in a foreclosure situation the bank holding the 2nd mortgage will likely get nothing. The bank would rather get 20 cents on the dollar than risk getting nothing. If the same bank owns both the 1st and the 2nd mortgages you are in the best possible scenario for a reduction. If they are owned by different banks then it things are a little more challenging. When a bank only owns the 2nd mortgage they will most likely to fight for whatever they can get. If your loans are owned by the same bank they will most likely be more concerned with getting the first into a manageable situation while viewing the 2nd as almost worthless.

Keep in mind that the banks DO NOT want to be in the real estate business. They don’t want to foreclose on a property in a declining market. In today’s market the banks stand to lose $0.35 to $0.80 on the dollar on any foreclosed property. If we were in a booming market the scenario would be more in the banks favor and you would most likely not be reading this post. Any bank would rather collect lower payments than none at all.

Next post we will discuss Negotiations…

Wednesday, January 21, 2009

Loan Modification Options

As discussed in the previous post, if you find yourself unable to make your current mortgage payments your options are foreclosure, deed in lieu of foreclosure, short sale or loan modification. The only option listed above that will allow you to stay in your home is the loan modification. Assuming that is your goal, you will need to be able to document your ability to repay the loan if some modifications to the terms are made. Some options that may be available are a temporary or possibly permanent interest rate reduction, or giving you an interest only payment option, modify your repayment terms from 30 years to 40 years or even 50 years, a principal balance reduction, a forbearance agreement or a combination of any of the above.

The Bank will take your entire budget into consideration including utilities, food, gas, credit card payments & cell phone bills. They don’t want your mortgage payment to consume your entire monthly income. You will need to complete an income vs expenses worksheet provided by your bank. Next post we will talk about principal balance reductions.

The Bank will take your entire budget into consideration including utilities, food, gas, credit card payments & cell phone bills. They don’t want your mortgage payment to consume your entire monthly income. You will need to complete an income vs expenses worksheet provided by your bank. Next post we will talk about principal balance reductions.

Monday, January 19, 2009

From the Banks Perspective

When Banks are first approached by a homeowner requesting help or a modification they may offer a quick fix that may end up hurting the homeowner in the end. These fixes would include a temporary rate cut (emphasis on “temporary”), a short sale, deed in lieu of foreclosure or a simple forbearance agreement. We will review each of these options as we go along. If you are willing to follow along with us here on this blog I believe you will reject any offer that will not fix your problem permanently.

Do You Refinance or Modify Your Loan?

In today’s economic environment most people do not qualify for a refinance making a loan modification their only option. You may have suffered a job loss and unable to replace the income you were used to making or you may be upside with your mortgage. Meaning, you owe more than the property is worth. Either way a modification is your only option. To be continued…

Do You Refinance or Modify Your Loan?

In today’s economic environment most people do not qualify for a refinance making a loan modification their only option. You may have suffered a job loss and unable to replace the income you were used to making or you may be upside with your mortgage. Meaning, you owe more than the property is worth. Either way a modification is your only option. To be continued…

Friday, January 16, 2009

Understanding Loan Modification