I read an article on Bloomberg.com by Alison Vekshin about a meeting that Sheila Bair, chairman of the FCIC had with President Obama. She is not a proponent of the too big to fail idea.

“The FDIC head isn’t done expanding her influence over Wall Street. An opponent of the “too-big-to-fail” policy for firms like Citigroup Inc., Bair is lobbying Congress to give the FDIC authority to wind down bank and thrift holding companies -- a move she says is necessary to protect taxpayers. And she wants lawmakers to include the agency in a systemic risk council to prevent future financial shocks.”

To read the entire article click here.

Friday, May 29, 2009

Tuesday, May 26, 2009

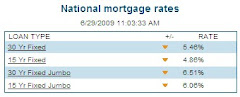

Job Losses Push Safer Mortgages to Foreclosure

As job losses rise, growing numbers of American homeowners with once solid credit are falling behind on their mortgages, amplifying a wave of foreclosures.

In the latest phase of the nation’s real estate disaster, the locus of trouble has shifted from subprime loans — those extended to home buyers with troubled credit — to the far more numerous prime loans issued to those with decent financial histories.

To read the full story click here

In the latest phase of the nation’s real estate disaster, the locus of trouble has shifted from subprime loans — those extended to home buyers with troubled credit — to the far more numerous prime loans issued to those with decent financial histories.

To read the full story click here

Thursday, May 21, 2009

Credit Reform

There are some changes being made on how credit card companies, Mastercard or Visa, approach college students and also some changes to how and when they can raise interest rates. It is designed to help consumers make more informed decisions on credit. Read the article below…

By ANNE FLAHERTY, Associated Press Writer Anne Flaherty, Associated Press Writer – Thu May 21, 5:54 am ET

WASHINGTON – It's an end of an era for the thousands of college students who rely on MasterCard or Visa to get them through tight times.

Under a new law awaiting President Barack Obama's signature, credit card companies will be prohibited from giving cards to people under 21 unless they can prove they have the means to repay the debt or a parent or guardian co-signs for the loan.

Congress passed the bill this week, and Obama was expected to sign it into law Friday. The changes will go into effect in nine months. "The hope is that when they spend, they'll spend under better terms and there'll be fewer traps for them," said Pedro de la Torre, a spokesman for Campus Progress, a progressive group in Washington that tracks issues affecting young people.

Congress is hoping to break a vicious cycle: A cardholder falls behind in paying the bill and watches helplessly as the interest rate spikes on the existing balance. Buried in higher rates and late fees, the cardholder spend less, which hurts local businesses.

To read the entire article click here

By ANNE FLAHERTY, Associated Press Writer Anne Flaherty, Associated Press Writer – Thu May 21, 5:54 am ET

WASHINGTON – It's an end of an era for the thousands of college students who rely on MasterCard or Visa to get them through tight times.

Under a new law awaiting President Barack Obama's signature, credit card companies will be prohibited from giving cards to people under 21 unless they can prove they have the means to repay the debt or a parent or guardian co-signs for the loan.

Congress passed the bill this week, and Obama was expected to sign it into law Friday. The changes will go into effect in nine months. "The hope is that when they spend, they'll spend under better terms and there'll be fewer traps for them," said Pedro de la Torre, a spokesman for Campus Progress, a progressive group in Washington that tracks issues affecting young people.

Congress is hoping to break a vicious cycle: A cardholder falls behind in paying the bill and watches helplessly as the interest rate spikes on the existing balance. Buried in higher rates and late fees, the cardholder spend less, which hurts local businesses.

To read the entire article click here

Monday, May 18, 2009

FED UP

Commentary

Fed Up

Ron Paul, 05.15.09, 07:10 PM EDT

Audit the Federal Reserve.

(found at forbes.com)

The Federal Reserve's recent and unprecedented actions in the realm of monetary policy have provoked a backlash among the American people. Trillions of dollars worth of loans and guarantees have been provided to Wall Street firms, while Main Street Americans suffocate under harsh taxation, the prospect of higher debt levels and increasing inflation. These events have awakened many Americans to problems with the Fed's loose monetary policy, the bubbles it has created in the past and the potential hyperinflation it might cause in the future.

One of the fallacies of modern economics is the idea that a central bank is required in order to keep inflation low and promote economic growth. In reality, it is the central bank's monetary policy that causes inflation and depresses economic growth. Inflation is an increase in the supply of money, which in our day and age is directly caused or initiated by central banks. All other things being equal, inflation results in a rise in prices. A so-called "mild" rate of inflation of 3% per year leads to a 56% rise in prices over a 15-year period. Even a "low" rate of inflation of 2% per year leads to a 35% rise over that same period. How is that conducive to long-term growth?

read more on this article

Fed Up

Ron Paul, 05.15.09, 07:10 PM EDT

Audit the Federal Reserve.

(found at forbes.com)

The Federal Reserve's recent and unprecedented actions in the realm of monetary policy have provoked a backlash among the American people. Trillions of dollars worth of loans and guarantees have been provided to Wall Street firms, while Main Street Americans suffocate under harsh taxation, the prospect of higher debt levels and increasing inflation. These events have awakened many Americans to problems with the Fed's loose monetary policy, the bubbles it has created in the past and the potential hyperinflation it might cause in the future.

One of the fallacies of modern economics is the idea that a central bank is required in order to keep inflation low and promote economic growth. In reality, it is the central bank's monetary policy that causes inflation and depresses economic growth. Inflation is an increase in the supply of money, which in our day and age is directly caused or initiated by central banks. All other things being equal, inflation results in a rise in prices. A so-called "mild" rate of inflation of 3% per year leads to a 56% rise in prices over a 15-year period. Even a "low" rate of inflation of 2% per year leads to a 35% rise over that same period. How is that conducive to long-term growth?

read more on this article

Friday, May 15, 2009

Deals abound but buyers frustrated, columnist finds

By SHANNON BEHNKEN The Tampa Tribune

Published: May 15, 2009

Ray White thought now was the perfect time to help his daughter buy her first home.

Home prices are more affordable than they have been in years, interest rates are low, there are plenty of homes on the market, and the federal government is offering an $8,000 tax credit.

But because of one problem after another, every house they find seems out of her reach — even though she's approved for a loan and has a down payment.

"The other night, she just broke down and cried," White said, noting that they've looked at more than 100 homes. "I actually have this feeling right now that it's almost impossible for her to buy a house."

That's partly because the Whites are competing with investors who often pay cash and then flip the property for big profit. They typically won't sell to those getting an FHA loan, which are very popular among first-time homebuyers.

Read More…

Published: May 15, 2009

Ray White thought now was the perfect time to help his daughter buy her first home.

Home prices are more affordable than they have been in years, interest rates are low, there are plenty of homes on the market, and the federal government is offering an $8,000 tax credit.

But because of one problem after another, every house they find seems out of her reach — even though she's approved for a loan and has a down payment.

"The other night, she just broke down and cried," White said, noting that they've looked at more than 100 homes. "I actually have this feeling right now that it's almost impossible for her to buy a house."

That's partly because the Whites are competing with investors who often pay cash and then flip the property for big profit. They typically won't sell to those getting an FHA loan, which are very popular among first-time homebuyers.

Read More…

Tuesday, May 12, 2009

Goldman to Pay $60 Million in Subprime Settlement (Update1)

The loan modifications aren't over. Not by a long shot. Read this article by Kathleen M. Howley and Christine Harper

May 11 (Bloomberg) -- Goldman Sachs Group Inc. agreed to pay about $60 million to settle a Massachusetts investigation into the packaging of mortgage securities at the root of the collapse of the U.S. housing market.

The agreement calls for the bank to pay about $50 million to compensate homeowners and the rest to the state, Massachusetts Attorney General Martha Coakley said today at a news conference in Boston. The deal will also allow for some loan principal reductions. Goldman Sachs directly holds 714 Massachusetts mortgages, she said.

The bundling of the riskiest type of mortgages into securities turned the U.S. housing slump into a global recession as foreclosures deflated bond values and toppled Wall Street firms such as Lehman Brothers Holdings Inc. The Massachusetts attorney general has investigated Fremont Investment & Loan, now defunct, and H&R Block Inc., owner of Option One Mortgage Corp., for making the types of mortgages that Goldman securitized. Read more...

May 11 (Bloomberg) -- Goldman Sachs Group Inc. agreed to pay about $60 million to settle a Massachusetts investigation into the packaging of mortgage securities at the root of the collapse of the U.S. housing market.

The agreement calls for the bank to pay about $50 million to compensate homeowners and the rest to the state, Massachusetts Attorney General Martha Coakley said today at a news conference in Boston. The deal will also allow for some loan principal reductions. Goldman Sachs directly holds 714 Massachusetts mortgages, she said.

The bundling of the riskiest type of mortgages into securities turned the U.S. housing slump into a global recession as foreclosures deflated bond values and toppled Wall Street firms such as Lehman Brothers Holdings Inc. The Massachusetts attorney general has investigated Fremont Investment & Loan, now defunct, and H&R Block Inc., owner of Option One Mortgage Corp., for making the types of mortgages that Goldman securitized. Read more...

Friday, May 8, 2009

Geithner Bets U.S. Can Avoid Japan Trap Through Bank Earnings

By Rich Miller and Matthew Benjamin

May 8 (Bloomberg) -- Treasury Secretary Timothy Geithner is betting that U.S. banks can do something their Japanese counterparts were unable to accomplish in that country’s “lost decade” of the 1990s: earn their way out of trouble.

The stress-test results released yesterday by regulators found that the 19 largest banks face a $74.6 billion capital hole that may be filled mostly by private money. That compares with the hundreds of billions of dollars seen by outside analysts, including the International Monetary Fund, and takes into account banks’ projected earnings over the next two years.

Read more…

May 8 (Bloomberg) -- Treasury Secretary Timothy Geithner is betting that U.S. banks can do something their Japanese counterparts were unable to accomplish in that country’s “lost decade” of the 1990s: earn their way out of trouble.

The stress-test results released yesterday by regulators found that the 19 largest banks face a $74.6 billion capital hole that may be filled mostly by private money. That compares with the hundreds of billions of dollars seen by outside analysts, including the International Monetary Fund, and takes into account banks’ projected earnings over the next two years.

Read more…

Monday, May 4, 2009

Mortgage Fraud Epidemic: How the FBI Blew It and Why There's No 'Perp Walks'

Posted Apr 06, 2009 08:00am EDT by Aaron Task

In the wake of the bursting of the housing bubble, you'd think there'd be a significant number of investigations into criminal wrongdoing and accounting fraud, similar to what occurred after the S&L crisis and bursting of the stock bubble in 2000.

But two years into the crisis the FBI "doesn't have a single major conviction or indictment of anyone," notes William Black, a former senior bank regulator and S&L prosecutor, and currently an Associate Professor of Economics and Law at the University of Missouri - Kansas City.

Black, who was counsel to the Federal Home Loan Bank Board during the S&L crisis of the 1980s and blew the whistle on the "Keating Five" in 1989, reiterated what he told us in November: Though the FBI warned of an "epidemic" of mortgage fraud in 2004, they subsequently made a "strategic alliance" with the Mortgage Bankers Association, which Black calls the "trade association of perps."

Read more…

In the wake of the bursting of the housing bubble, you'd think there'd be a significant number of investigations into criminal wrongdoing and accounting fraud, similar to what occurred after the S&L crisis and bursting of the stock bubble in 2000.

But two years into the crisis the FBI "doesn't have a single major conviction or indictment of anyone," notes William Black, a former senior bank regulator and S&L prosecutor, and currently an Associate Professor of Economics and Law at the University of Missouri - Kansas City.

Black, who was counsel to the Federal Home Loan Bank Board during the S&L crisis of the 1980s and blew the whistle on the "Keating Five" in 1989, reiterated what he told us in November: Though the FBI warned of an "epidemic" of mortgage fraud in 2004, they subsequently made a "strategic alliance" with the Mortgage Bankers Association, which Black calls the "trade association of perps."

Read more…

Subscribe to:

Comments (Atom)